The types of digital fraud threats that businesses face in 2025 and early 2026 are becoming increasingly sophisticated. For example, deep fakes can spoof a user’s ID and gain access to sensitive data, which is why liveness detection to stop deepfakes is becoming essential.

For businesses, fraud and identity theft can cause severe damage to their finances and reputations. The financial risks are clear.

According to the Federal Trade Commission (FTC), total reported fraud losses in the United States reached $15.9 billion in 2025.

For customers, identity theft and identity fraud can also have devastating consequences. To effectively combat fraud, it is crucial to understand the issues and their impact on your customers.

It has never been more crucial for businesses to be vigilant and aware of evolving fraud threats, know best practices, and implement strong identity verification solutions. Businesses should take proactive steps to help keep customers secure and fight against digital identity fraud.

In this guide, we’ll explore common types of digital fraud, why traditional prevention methods are struggling to keep up, and the strategies businesses can use to strengthen fraud detection and identity verification in 2026.

Why Traditional Fraud Prevention is Failing

The evolution of cybercrime and online fraud has revealed that security measures that once prevailed everywhere are no longer safe and are easily trespassed upon by cyber attackers.

Let’s talk about the major reasons for fraud prevention failure.

Static Passwords Are Outdated

In the era of the rise of advanced technology like brute-force tools and AI-driven credential stuffing, the password seems to be a weak point in securing the account. These passwords can be breached in seconds by attackers, and it doesn’t always serve the real purpose of keeping the invaders out.

OTP Fatigue Attacks

Multi-factor authentication (MFA) has served the safety purpose so far; however, attackers have found a new way, i.e., a psychological attack, also known as an OTP fatigue attack.

Fraudsters will bombard continuous push notifications or one-time passcodes (OTPs) in the middle of the night, and at some point, instead of ignoring them, someone will click the notification to make it stop, purely out of frustration, and this click gives them the whole access to your private account.

What’s meant to be a security safeguard can end up being used as pressure, turning authentication prompts into a tool for manipulation rather than protection.

Rule-Based Systems vs. AI Fraud

A traditional method of fraud prevention is an “if-then” rule where certain rules are applied to flag the process as risky. E.g., if an internet protocol (IP) address is from a different country, flag the transaction.” Although modern criminals use AI to test such rules and find the loophole or blind spot to invade them.

On the other hand, AI-powered fraud detection doesn’t wait for a rule to be broken and analyzes the user’s behavior and matches it with the accessing user, finding discrepancies. This behavior includes the typing style of the user, mouse movements, unique device fingerprints, etc.

Rule-based systems look for what is entering, and AI-based systems look at how it’s entering, catching the invaders efficiently.

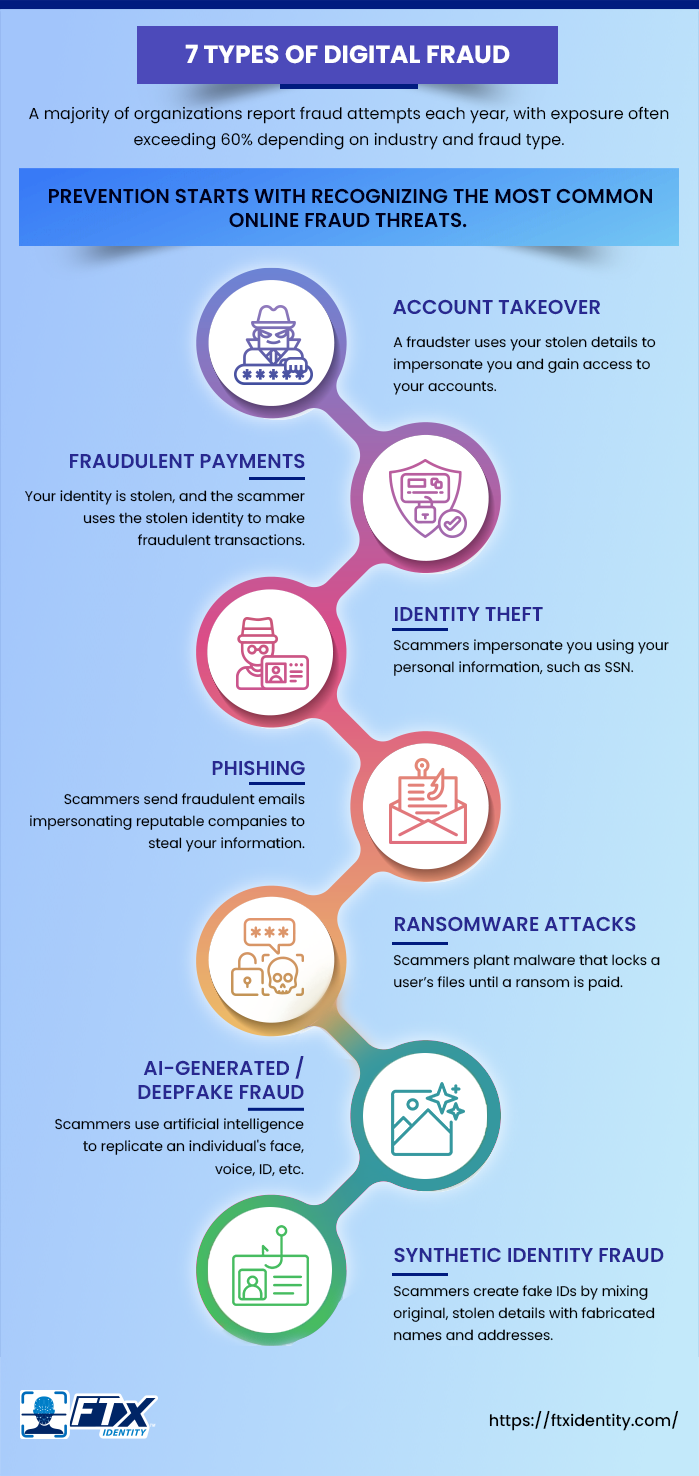

Types of Digital (Online) Fraud

Online fraud has grown alongside digital payments and remote work, shifting from simple scams to more automated and harder-to-detect attacks.

Today’s fraud is more advanced, with criminals using tools like AI and automation to make scams more convincing and harder to trace, often across borders.

As a result, online fraud continues to impact both businesses and consumers worldwide.

That’s why strong digital identity verification and fraud prevention tools are more important than ever.

The first step in staying protected is understanding the most common types of online fraud.

Here are seven to watch for in 2026:

1. Account Takeover

Account takeover occurs when an unauthorized individual gains access to a user’s account. Once they gain access, scammers can impersonate you using your details, steal money, make unauthorized transactions, and misuse your card details.

Account takeover (ATO) fraud continues to rise as cybercriminals increasingly shift from stealing identities to hijacking existing accounts. According to TransUnion, 5.1 million U.S. adults were affected by account takeover fraud in 2024.

Methods:

The scammers lure you into disclosing your credentials or personal information by various methods, such as:

- Stealing your passwords and breaching your security questions

- Making fake phone calls claiming to be bank executives

- Sending fake bank messages, for example, “Your account information is incomplete; please contact us to avoid account closure”

- Emailing fake website links that hack all the information once clicked or logged in

2. Fraudulent Payments

This refers to financial fraud, where scammers have made fraudulent financial transactions.

Statistics:

- Global e-commerce fraud losses are projected to increase from approximately $56 billion in 2025 to $131 billion by 2030, representing a growth of over 130%. (Juniper Research)

- 26% of consumers reported losing money due to digital fraud. (TransUnion)

- In 2025, 76% of organizations were impacted by attempted or actual payment fraud. (Association for Financial Professionals (AFP))

Method:

Scammers can gain access to accounts and make fraudulent payments by:

- Using the stolen credit card information

- Issuing new credit cards and making transactions

- Issuing fake checks

- Making online fund transfers

3. Identity Theft

A type of online crime where a scammer tries to impersonate you by using your personal information, such as name, social security number, etc., for unauthorized acquisitions, such as financial gain.

Identity theft often results in long-term financial harm, with the Identity Theft Resource Center reporting that 36.9% of victims experienced losses exceeding $10,000.

Warning Signs:

- Check for unauthorized purchases

- Scan your bills before making payments for any items you did not buy

- If you received a call confirming the purchase of a new credit card

- New logins in your social media apps from unknown locations (you can find them in settings)

- New loan accounts created on your account name

Methods of ID theft:

- Data breaches

- Weak passwords

- Scooping trash bins for account information

- Impersonating a financial officer to gain account details

- Fake lottery winning, job placement forms, or online forms

- Rig the devices at ATMs

4. Phishing

Cybercriminals have used this old but highly effective (and still widely used) technique for ages, sending deceptive emails or messages impersonating reputable companies to obtain personal information.

- Phishing attacks reached 3.8 million in 2025, a slight increase from 3.76 million in 2024 (APWG)

- In the first quarter of 2025, the Anti-Phishing Working Group (APWG) recorded 1,003,924 phishing attacks, the highest quarterly total in recent years. (APWG)

- In Q1 2025, attacks on the online payments and banking sectors increased, accounting for 30.9% of all attacks. (APWG)

Methods:

a. Spear Phishing – You receive a malicious email. For example, a security alert email, such as, “Your account has been compromised.”

b. Email Phishing – You receive fake emails asking you to complete an action, like a fake invoice scam, a message from the HR team to fill out a job document, or a taxing department to click on a link to avoid tax.

c. Vishing – Vishing is short for “voice phishing” that involves defrauding people by pretending to be a person of high authority. For instance, a law enforcement officer asking for your personal details or a fraud investigator asking for account details.

d. Link Manipulation – This type of phishing involves scammers sending viruses through links or retracting account information by sending wrong links.

5. Ransomware Attacks

Ransomware attacks are malicious malware that attack the user’s personal files and lock them out unless a ransom is paid. This type of attack generally targets influential individuals or big conglomerates. Once the ransom is paid, these cybercriminals give back access (but in most cases, they damage the files even after the ransom is paid).

How It Works

- Cybercriminals create malware software

- The malware infiltrates the victim’s system, further encrypting the files

- The criminals demand ransom in exchange for the decryption key

- Once the ransom is paid, they grant the victim access to all the files and data

2025-2026 Ransomware Attacks:

- In 2025, Yale New Haven Health suffered a ransomware attack that compromised data for nearly 5.6 million patients, including personal and medical information. The breach led to operational disruption and long-term legal and compliance consequences (TechTarget).

- In 2026, education technology provider Instructure, which operates the Canvas learning platform, reported a ransomware-related security incident involving unauthorized access to its systems. The attack caused temporary service disruption and raised concerns about potential exposure of user data, including student and institutional information (Wired).

- In a major 2025 incident affecting millions of students and teachers across North America, PowerSchool, a K–12 SaaS provider, suffered a ransomware-related breach involving unauthorized access to student information systems and the exposure of sensitive data (TechCrunch)

6. AI-Generated / Deepfake Fraud

AI-generated fraud is the use of the latest tech to achieve the goals of cyber-loot. Generative adversarial networks (GANs) are used to create realistic video, audio, or image clones of legitimate person.

How It Works:

First, fraudsters scan and collect the public media from the social media platforms and train the AI model, and then they use these deepfakes for the video KYC (Know Your Customer) checks or live video identity verifications.

As AI blinks, speaks, and reacts in real-time, it can breach the live detection tests that aren’t equipped with advanced features like texture and pulse rate analysis.

7. Synthetic Identity Fraud

Synthetic identity fraud means stitching together real and fake information, creating a completely new person, which is also known as “Frankenstein fraud.”

How It Works:

A criminal combines real details that were stolen earlier, like Social Security Number, with fake details like a name, address, and birthdate.

Then combines them to make a full identity document and uses this person to open accounts and builds the positive credit score for a significant amount of time, and there is no one to report the identity theft so far.

Then one day, the fraudster takes a massive loan or empties the credit lines and disappears. It’s already done when systems realize that the person never existed.

How Digital Fraud Detection Strengthens Trust and Security

Fraud prevention is not just a defensive wall, but it also offers a competitive advantage to the organization by giving a strong foundation to protect digital transactions and communication. The digital fraud detection simply offers the following benefits that have remained underrated so far.

Protecting Finances

The digital fraud detection with AI gives the most important benefit that is protecting your finances in more than one possible way. Mainly, the businesses are in a “reactive” position, where they act after the fraud happens, but with fraud detection capabilities, they turn into a “proactive” position where they can stop the transaction before it happens.

It saves the money before it goes out and saves the administration fees and legal penalties associated with the recovered funds.

Preserving Customer Trust

Customer trust is one of the most important assets in the digital economy. When customers are aware that their identity is protected by sophisticated tools like FTx Identity, they feel secure and transact frequently.

On the other hand, a single security breach is enough to ruin the years of brand loyalty. Modern fraud detection is a silent warrior, ensuring the safety of the transactions and smooth experiences.

Ensuring Regulatory Compliance

The mandates like the General Data Protection Regulation (GDPR), California Consumer Privacy Act (CCPA), and Anti-Money Laundering (AML) directives require the businesses to prove that they are maintaining the reasonable safety standards to verify identities.

A strong fraud detection provides an automated audit trail that ensures your business remains compliant with international laws. It simply avoids large fines associated with regulatory failures.

Maintaining Operational Efficiency

Manual reviews mainly take and sometimes waste time of the business and of the customer. Human nature is built in such a way that they always suspect everything slowing down the transaction and sign-up processes. AI-driven fraud detection speeds up the task and automatically does the process with utmost accuracy. That ultimately allows human resources to focus on other important functions.

Securing Data

Securing data with various measures such as encryption makes it inaccessible to unauthorized users. This practice helps in effective detection of fraud at an early stage avoiding account takeover and data theft. By halting the attackers at the entrance, the integrity of your database remains protected.

Supporting Market Stability

At a bigger level of the business world, when the data is protected digitally and fraud is prevented with secure measures, it supports the businesses to grow together where their practices are trusted and considered safe. The entire digital economy functions smoothly, predictably, and creates a safe environment for businesses as well as users.

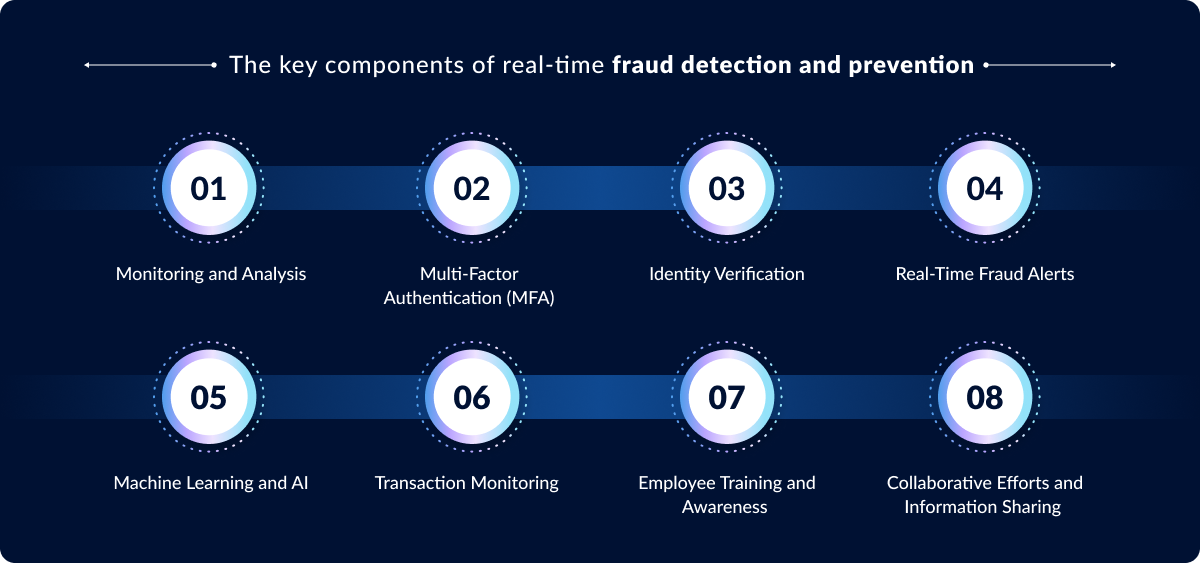

What Is Fraud Detection and Prevention?

Fraud detection and prevention refers to strategies and technologies constantly fighting to identify and mitigate fraudulent activities. The most targeted industries are banking, finance and insurance, e-commerce, public or government companies, retail, etc.

The key components of real-time fraud detection and prevention:

1. Monitoring and Analysis

2. Multi-Factor Authentication (MFA)

3. Identity Verification

4. Real-Time Fraud Alerts

5. Machine Learning and AI

6. Transaction Monitoring

7. Employee Training and Awareness

8. Collaborative Efforts and Information Sharing

Digital Fraud Prevention Techniques (Strategies to Use)

Here are some of the most reliable digital fraud strategies:

1. Stop Relying on Passwords

Passwords are no longer necessary. It is now a matter of when corporations will stop using passwords in favor of emerging technology like biometrics, with many, if not most, businesses moving away from them soon.

Users find passwords annoying, and they need to be a more secure solution. Although they have always been used online, passwords have become misused.

For example, they are increasingly used as identification documents when signing contracts or conducting business. In this instance, a stolen password allows someone to sign on your behalf. One-time passwords (OTPs) used as a multi-factor authentication (MFA) component are susceptible to incidents like SIM swapping and scammers pressing victims for codes.

2. Use Two-Factor Authentication

Two-factor authentication (2FA) adds an extra security layer to businesses and is relatively easy to implement.

Here’s how it works: When users log in, they first enter their password. That’s step one. For step two, they need to provide another proof of identity. This could be a code sent to their phone or an app. So, even if someone steals the password, they can’t get in without the second factor.

Businesses can use 2FA to protect sensitive data like customer information or financial records. It’s easy to set up. Many online services offer 2FA as a feature. Just be sure to train your employees in how to use it. Remember, 2FA is not foolproof. But it makes it much harder for hackers to steal sensitive data. It’s a simple, effective way to boost your business’s security.

For more on authentication, see our guide: Identity Verification vs. Authentication: Understanding the Key Differences

3. Transition to Biometrics

Biometric authentication boosts security for businesses. It uses unique features like fingerprints or facial recognition, which are nearly impossible to steal, unlike passwords.

Another advantage: Biometrics are user-friendly. They don’t need to be remembered or updated. This reduces the risk of data leaks and security breaches, and it also gets rid of password fatigue. Users often reuse or choose weak passwords. Biometrics doesn’t have this problem. They also work faster than passwords and make things more efficient.

However, using biometric authentication does have its challenges. These include privacy issues and the risk of physical theft. If biometric data is compromised, it’s hard to change. So, a balanced approach with multiple security layers is best.

4. Use Secure Networks

Secure and trusted networks are essential for businesses when conducting online transactions. Here’s why:

- Secure networks encrypt data: The information sent and received is encrypted when businesses use secure networks. This makes it difficult for cybercriminals to intercept and misuse the data.

- Trustworthy networks reduce risk: Trusted networks have security measures to protect against malware or phishing attacks. Using these networks minimizes the risk of such attacks.

- Customer confidence: Customers want assurance that their sensitive information, like credit card details, is safe. Using secure networks for transactions boosts customer confidence and trust in the business.

- Regulatory compliance: Many industries have regulations requiring secure networks for transactions. Compliance helps avoid penalties and maintains a business’s reputation.

In summary, using secure and trusted networks for online transactions is vital to a business’s cybersecurity strategy. It protects the company and its customers, enhancing trust and compliance with regulations.

5. Focus on Data Transparency

Data transparency is the first step in easing consumer adoption of biometrics. Companies must be transparent about the types of customer information they collect and how they plan to use it. Additionally, they must offer a way for individuals to express their permission to use that biometric and the option to change their minds at any time.

Consumers want to feel confident and secure when it comes to how biometrics are used—whether by governments, businesses, AI systems, or even social platforms. Building that trust means being transparent, supporting users, and helping them understand how biometric data is handled under evolving regulations.

For example, the AI Bill of Rights, which safeguards personal information and biometrics.

Consumers can feel secure committing their digital security to biometric-based authentication solutions with this knowledge and unambiguous communication from a reliable service provider. The decision to employ biometrics ultimately rests with the customer, who must be well-informed to make the best choice.

6. Build Customer Trust

You must build trust with your customers as you transition to new processes. You are responsible for informing customers of what new platforms entail. Businesses must, after all, serve as the first line of defense in the fight against digital fraud.

Nowadays, the consumer employs unique and non-transferable values when using biometrics on mobile devices, eliminating the inconveniences of forgetting passwords, attempted fraud, and missing coverage.

If the person knows this, they can guarantee security and excellent user experience. Creating easy-to-use, safe, clear, and highly secure biometrics will encourage customers to use them instead of passwords.

To further improve customer security, businesses should educate customers on safeguarding their personal data and identity online.

Companies could share easy victories with their customers, such as securing your home network with strong passwords and encryption, turning off or locking your work computer when you’re not using it, and being cautious when clicking links in emails.

7. Educate Your Customers

Businesses must notify customers about fraud schemes that pose a threat and educate them about securing their identity and employing biometrics for added security. As an example, the use of voice calls by fraudsters to obtain information or persuade victims to give them access to their money is on the rise.

They pose as banks or governmental agencies while knowing just enough about the customer to convince them there is a problem with their account and trick them into disclosing account information, resulting in digital banking fraud.

Customers’ personal information is frequently used by fraudsters in account takeover (ATO) operations. They call customer service centers to take over the account and pose as the customer. However, in these situations, the customer could prevent this kind of attack if they had voice biometrics set up.

8. Real-Time Monitoring

Continuous monitoring helps businesses identify suspicious behavior and potential threats. It’s also commonly used for identity verification in fintech. It involves real-time system observation to detect anomalies and potential threats. For example, this is a powerful tactic to catch synthetic identity fraud.

Here’s how it works:

a. Businesses install monitoring systems to track activities across their networks.

b. These systems continuously scan for unusual behavior, repeated verification failures, or suspicious patterns.

c. If an anomaly is detected, alerts are triggered for immediate action.

d. This allows businesses to respond to threats before they cause harm.

e. This is one of the best ways to find and address threats quickly, and it’s widely used to monitor customer and employee data.

How FTx Identity Helps Prevent Online Fraud

Fraudsters are constantly evolving their tactics, using new tools and methods to bypass traditional security measures. That’s why businesses need identity verification that adapts just as quickly.

FTx Identity strengthens fraud prevention by moving beyond passwords and static authentication to a biometric-first approach. This helps verify that users are who they claim to be in real time, reducing the risk of account takeover, unauthorized access, and fraudulent transactions.

By embedding identity verification directly into the authentication process, FTx Identity helps businesses secure their digital ecosystem without adding unnecessary friction for legitimate users.

The result is stronger protection against modern fraud attempts and a more secure foundation for digital transactions.

Conclusion

Identity verification and fraud prevention are changing quickly, and staying ahead of fraudsters means keeping pace with that change. It takes a proactive, AI-driven approach that goes beyond traditional security measures and adapts as threats evolve.

The key point is simple—you don’t need to wait for a breach to find out if your system is secure. Modern protection should already meet today’s security standards before attackers ever get the chance to test them.

Get in touch today to schedule a consultation and see a demo.